From Unbanked to Entrepreneurs: AI Credit Scoring Breaks Financial Barriers

The Day a Woman Got Her First Loan: AI Making Financial Dreams Real For 30 years, Amina had dreamed of expanding her small textile business beyond her street-side stall in Lagos, Nigeria. She had experience, reliability, and a track record of consistent income. But when she approached traditiona

The Lankawebsites editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lankawebsites readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

The Day a Woman Got Her First Loan: AI Making Financial Dreams Real

For 30 years, Amina had dreamed of expanding her small textile business beyond her street-side stall in Lagos, Nigeria. She had experience, reliability, and a track record of consistent income. But when she approached traditional banks for a loan, she was turned away. No formal credit history. No collateral. No paperwork proving her creditworthiness. The banks had no way to assess her as a borrower.

Three years ago, that rejection would have meant the end of her expansion dreams. Today, Amina accessed a microloan through a fintech platform using AI credit scoring powered by alternative data. The algorithm analyzed her mobile money transaction patterns—showing her consistent cash flow—her utility payment history, her behavior in the app. The result: approved for a loan larger than she’d ever qualified for through traditional banking. She expanded her business, hired two additional workers, and tripled her annual income.

Amina’s story is one of 65+ million. A woman in Kenya accessing working capital for her fruit and vegetable wholesaling business through mobile data analysis. A shopkeeper in Indonesia receiving inventory financing based on transaction patterns. A farmer in Egypt approved for agricultural input loans analyzed from utility bill payment consistency. A young man in India qualifying for business expansion credit based on e-commerce seller ratings.

These aren’t isolated successes. They represent a fundamental shift in who gets access to capital—and who becomes able to build wealth. Artificial intelligence-powered credit scoring is breaking the financial barriers that have kept 1+ billion people excluded from formal banking. Where traditional credit systems see risk (no credit history = too risky), AI systems see opportunity (alternative data = reliable signal of creditworthiness).

The Financial Exclusion Crisis

To understand AI credit scoring’s impact, we first need to understand the problem it solves: the brutal reality of financial exclusion.

1+ billion adults globally lack access to formal financial services. This isn’t just an inconvenience—it’s a poverty trap. Without access to credit, poor people have no way to invest in their futures. A farmer can’t buy better seeds. A trader can’t expand inventory. A young person can’t start a business. Each generation remains trapped in the same economic circumstances as the previous.

The statistics are stark:

- In Sub-Saharan Africa, 57% of adults are unbanked

- In South Asia, 75% of adults lack formal financial services

- Globally, women are disproportionately excluded (about 20% more likely to be unbanked than men)

- Rural populations have access rates 50%+ lower than urban populations

Why are so many people excluded? The fundamental reason: traditional credit systems require evidence that doesn’t exist for poor people.

Traditional Credit System Requirements:

- Credit history (3+ years of formal borrowing and repayment)

- Collateral (physical assets like land or property worth 125%+ of loan value)

- Formal income documentation (tax returns, formal employment contracts)

- Stable address and identification verified through government systems

For a person living in a developing country’s rural area, none of these exist. They’ve never had a formal loan—so no credit history. They own only the clothes they wear—so no collateral. They work informally or farm—so no tax returns. Their address might be a rural settlement with no formal address system.

By the traditional metrics, they’re “unbanked for good reason”—too risky. Banks can’t justify the administrative costs of lending to someone with no verifiable track record. The result: billions of capable, entrepreneurial people are locked out of capital markets entirely.

The cost of exclusion is enormous:

- Microenterprises (the primary income source for 300+ million people globally) operate with severely limited capital

- Entrepreneurs with good ideas can’t execute them

- Women entrepreneurs are particularly disadvantaged, with 5+ million estimated annually denied financing

- Communities remain trapped in poverty because wealth-building requires capital

- Economic potential goes unrealized—the World Bank estimates a $5+ trillion finance gap for MSMEs

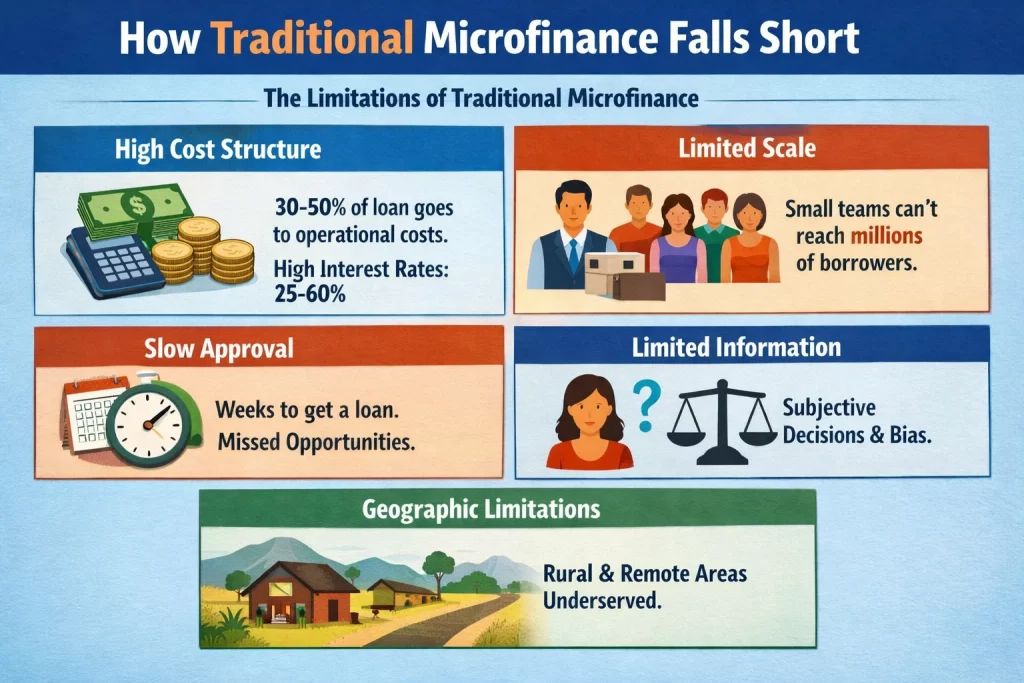

How Traditional Microfinance Falls Short

For decades, microfinance was positioned as the solution to financial exclusion. Microfinance institutions (MFIs) specialized in lending small amounts ($50-500) to poor entrepreneurs, replacing banks’ formal requirements with relationship-based lending and group accountability.

Microfinance helped millions. But it had critical limitations:

High Cost Structure: Traditional microfinance lending involves human relationship-building, field agents visiting borrowers, manual documentation, and slower approval processes. These costs are expensive. MFIs spend 30-50% of loan amount on operating costs. For a $100 microloan, $30-50 goes to operational costs. That means the borrower pays much higher interest rates (25-60% annually) to cover costs.

Limited Scale: Relationship-based lending doesn’t scale beyond a certain point. One loan officer can manage perhaps 500-1,000 borrowers. To serve millions requires armies of loan officers—expensive and geographically limited.

Slow Approval: A microloan approval took weeks. A borrower needing working capital urgently—because they found an opportunity to buy inventory—faced a dilemma. The opportunity passed while they waited for approval.

Limited Information: Loan officers made decisions based on character assessment and local knowledge. While this had value, it was also subjective and vulnerable to bias. A woman borrower might be deemed “too risky” based on gender despite being fully capable of repaying.

Geographic Limitations: Microfinance concentrated in areas with populations dense enough to support field agents. Remote rural areas remained underserved because the operating cost per borrower was simply too high.

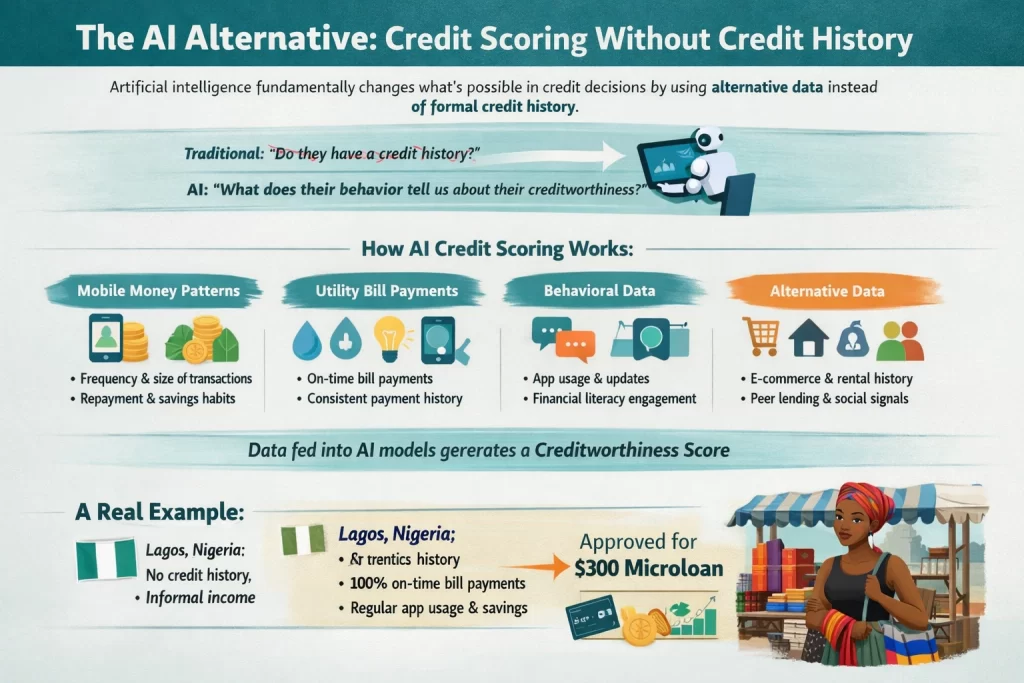

The AI Alternative: Credit Scoring Without Credit History

Artificial intelligence fundamentally changes what’s possible in credit decisions by using alternative data instead of formal credit history.

How AI Credit Scoring Works:

Instead of asking “Does this person have a credit history?”, AI asks “What does this person’s actual behavior tell us about their creditworthiness?”

The algorithm analyzes digital data trails—the evidence of a person’s financial behavior:

Mobile Money Transaction Patterns:

- Frequency of transactions (someone making 3-4 transactions weekly vs. 1-2 monthly shows different cash flow characteristics)

- Transaction size patterns (someone consistently sending $50-100 to family shows reliability; erratic patterns suggest instability)

- Repayment patterns (if someone borrowed from a peer and repaid, that’s evidence of reliability)

- Savings patterns (someone regularly depositing money shows financial discipline)

Utility Bill Payment History:

- On-time electricity, water, or phone bill payment shows financial discipline

- Consistent payment pattern is strong evidence of reliability

- Late payments might indicate cash flow problems

Behavioral Data from Apps:

- How frequently the person uses financial services

- Whether they keep their app updated

- How they interact with support services

- Whether they read financial literacy materials

Alternative Financial Data:

- E-commerce seller ratings and transaction history

- Rental payment history (if available)

- Peer lending data (through platforms like Kiva)

- Social media verification and data

Psychometric Assessment:

- Analysis of communication patterns revealing reliability

- Quiz responses about financial decision-making showing financial literacy

When fed into machine learning models trained on millions of historical borrowers, these data points generate a creditworthiness score without requiring any formal credit history.

A Real Example:

A woman in Lagos, Nigeria had been rejected by traditional banks:

- No credit history (never borrowed formally)

- No collateral (rents her home)

- No formal income documentation (sells textiles from street stall)

But she had been a Halan app user for 2 months. The AI algorithm analyzed:

- 47 transactions totaling $850 (shows cash flow)

- 100% on-time utility bill payments for 18 months (shows financial discipline)

- Daily app usage, consistent engagement (shows financial interest)

- High savings rate relative to income (shows financial priorities)

Result: Approved for a $300 microloan. From there, she was approved for the Halan Card (digital payment card) and later accessed investment products—a complete financial journey enabled by AI.

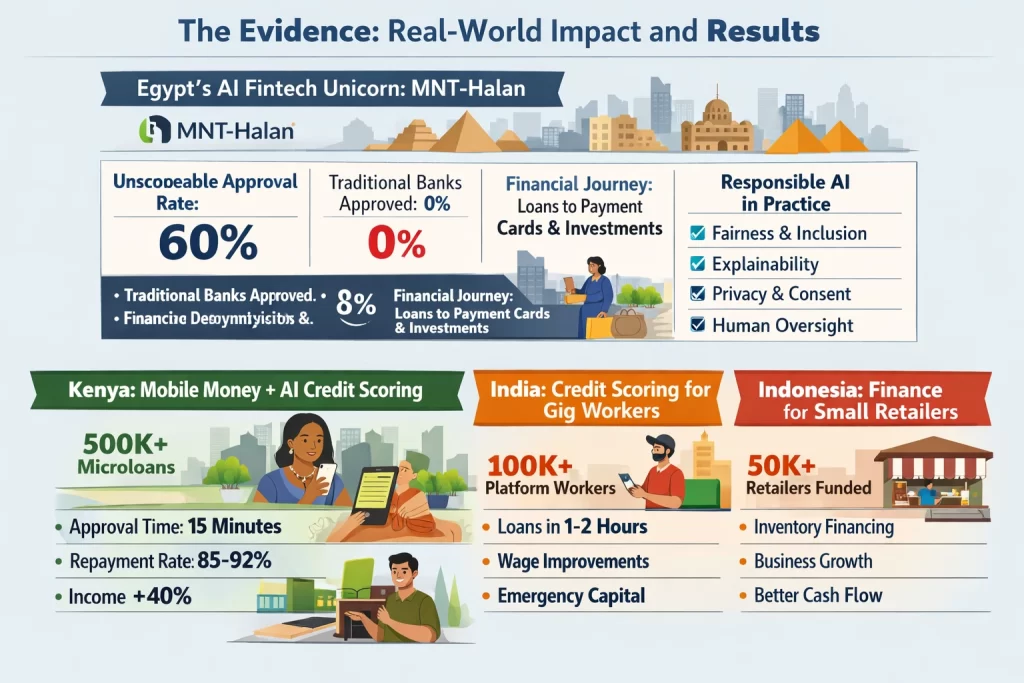

The Evidence: Real-World Impact and Results

AI credit scoring isn’t theoretical. It’s operational at massive scale right now, with proven results.

Egypt’s AI Fintech Unicorn: MNT-Halan

Egypt’s fastest-growing fintech, MNT-Halan, epitomizes AI credit scoring’s potential. The company built an AI engine analyzing behavioral and transactional data rather than credit history. Results from 65M+ people served:

Approval Rate for Previously Unscoreable Users: 60%

- Traditional banks would have approved: 0% (no data)

- AI-powered system: 60% approval rate for previously “unbanked” users

- This isn’t approval of high-risk borrowers—these are capable people with data signals of creditworthiness that formal systems never captured

Full Financial Journey: Instead of one-time loans, AI scoring enables a progression:

- First loan (consumer finance, $200-500)

- Graduation to digital payment card

- Access to investment products

- Secured credit products

- Long-term wealth-building

Responsible AI in Practice: Crucially, MNT-Halan didn’t just maximize approvals—they built fairness into their system:

- Fairness: Models explicitly include unbanked users; continuous bias monitoring across segments

- Explainability: Transparent scorecards showing which data points matter and how much

- Privacy: All data collected with user consent; users can opt out

- Monitoring: Continuous model updates based on real-world performance

- Human Oversight: Sensitive cases reviewed manually to ensure automation doesn’t override judgment

Financial Literacy:

- Personal finance education integrated into platform

- Users understand their credit scores and how to improve them

- Financial decision-making supported by educational tools

Scaling Across Region: Expansion to Turkey, Pakistan, UAE, targeting 64% unbanked adult population across Arab region (only 29% of women have accounts)

Kenya: Mobile Money + AI Credit Scoring

In Kenya, where mobile money (M-Pesa) is ubiquitous, fintech platforms analyze mobile transaction data to make credit decisions. A woman with 2+ years of consistent mobile money history—sending money to family, receiving payments for goods sold, savings pattern—is assessed as creditworthy.

Results:

- Microloans to 500,000+ previously unbanked people

- Average loan amount: $200 (working capital for retail traders, farmers, craftspeople)

- Approval time: 15 minutes (vs. weeks for traditional microfinance)

- Repayment rates: 85-92% (comparable to or better than formal banking)

- Income improvement: 40% average increase year-over-year for borrowers

- Job creation: Successful microenterprises create employment for family members

India: Credit Scoring for Digital Platform Workers

Platforms like KarmaLife provide credit to gig workers (delivery drivers, freelancers, platform sellers) using transactional data from the platforms themselves. A delivery driver’s earnings history, cancellation rate, customer ratings become the credit assessment.

Results:

- 100,000+ gig workers accessing working capital

- Loan approvals in 1-2 hours (vs. impossible through traditional banking)

- Usage: Vehicle maintenance, temporary capital for emergencies

- Wage improvements: Access to credit reducing reliance on predatory lending

Indonesia: Embedded Finance for Small Retailers

Fairbanc uses AI to assess creditworthiness of small retail shop owners based on inventory turnover, transaction data from their point-of-sale systems, and customer transaction patterns.

Results:

- 50,000+ retailers access inventory financing

- Inventory expansion without high-interest informal lending

- Business growth from better inventory management

- Retailers moving from survival mode to growth mode

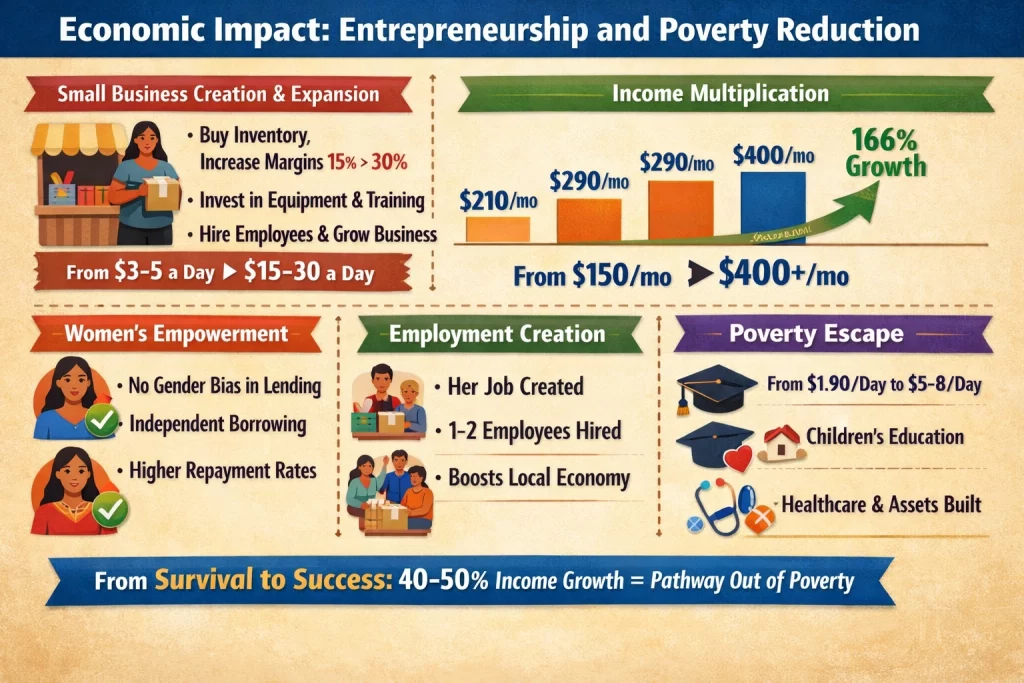

Economic Impact: Entrepreneurship and Poverty Reduction

The true measure of AI credit scoring’s impact isn’t the number of loans—it’s what those loans enable.

Small Business Creation and Expansion: A woman with $500 can:

- Buy wholesale inventory, increasing retail margins from 15% to 30%

- Supply her business with better tools/equipment

- Hire help, transitioning from solo survival to managed growth

- Invest in skills training for herself or employees

The result: a microenterprise transitions from survival business (earning $3-5 daily) to genuine small business (earning $15-30 daily, employing others).

Income Multiplication: For a borrower earning $150/month from self-employment:

- Year 1: Loan enables inventory expansion, income rises to $210/month (40% increase)

- Year 2: Successful repayment enables larger loan, income rises to $290/month

- Year 3: Business legitimacy enables formal business registration, access to additional services, income reaches $400/month

- Year 5: From $150/month to $400+/month (166% increase)

Women’s Empowerment: AI credit scoring particularly benefits women because:

- Removes subjective gender bias in assessment (algorithm doesn’t discriminate based on gender)

- Recognizes women’s actual financial behaviors (savings patterns, bill payment, household cash management)

- Enables independent borrowing (no male co-signer required)

- Supports women’s business independence

Global data shows women borrowers through AI platforms show:

- Higher repayment rates than men (women more financially disciplined)

- Significant income growth (40-50% year-over-year typical)

- Multiplier effects on families (women invest earnings in children’s education, household stability)

Employment Creation: A woman accessing a $300 loan for inventory typically creates:

- Her own job (business becomes legitimate employment)

- 1-2 additional jobs (hires helpers or family members)

- Indirect employment (wholesale suppliers gain business)

- Multiplier effect through local economy

Poverty Escape: Income growth of 40-50% year-over-year, sustained over 3-5 years, is transformative:

- Movement from extreme poverty (

3.20/day)

- From moderate poverty to lower-middle income ($5-8/day)

- Ability to invest in children’s education (breaking poverty cycles)

- Healthcare access (no longer forced to choose between medication and food)

- Asset building (home improvement, tools, inventory)

The Mechanism: Why Alternative Data Works

Why is AI credit scoring effective when formal credit history isn’t available?

The key insight: Creditworthiness is about behavioral consistency, not formal history. Traditional credit scores measure behavior within the formal financial system. AI scores measure behavior period.

A woman who pays her electricity bill on time every month is demonstrating financial responsibility. A trader who sends consistent remittances to family shows reliability. A farmer who saves regularly shows financial discipline. These behaviors predict loan repayment just as well as (or better than) formal credit scores.

Why Traditional Systems Missed This: Banks couldn’t see this alternative data. It wasn’t aggregated, digitized, or accessible. A woman’s utility payment history existed only in paper files with the utility company. Her mobile money transactions existed in her mobile provider’s database. No single institution had the data, so no institution could analyze it.

Why AI Can Leverage This Data: Modern AI systems can:

- Access diverse data sources (with consent): Mobile data, utility companies, app usage, e-commerce platforms

- Synthesize across sources: Combine utility, mobile, app, and transactional data into comprehensive picture

- Find predictive patterns: Machine learning identifies which behaviors actually predict repayment

- Process at scale: Analyzing millions of data points for millions of people, constantly improving predictions

The Accuracy is Impressive: Research shows AI credit scoring using alternative data achieves:

- Similar or better default prediction compared to traditional credit scores

- Broader approval without deteriorating quality (doesn’t just approve higher-risk borrowers)

- Fairness improvements when built carefully (reduces some forms of bias)

Implementation Challenges: Real Barriers to Scaling

Despite impressive potential, AI credit scoring faces real barriers to scaling across developing countries.

Challenge 1: Data Availability and Privacy

In some countries, the required data isn’t readily available. Utility companies don’t digitize records. Mobile providers guard data jealously. E-commerce platforms operate in silos. Even where data exists, privacy regulations might prevent access.

Solutions Emerging:

- Government digital infrastructure investment (India’s Aadhaar biometric ID, UPI payment system)

- Open banking regulations requiring data sharing with consent

- Platforms aggregating multiple data sources (superapp models like Halan integrating payments, savings, e-commerce)

- Privacy-preserving technologies (federated learning where algorithms run on devices, data stays private)

Challenge 2: Data Quality and Bias

Alternative data isn’t always reliable. A mobile transaction might indicate cash flow or might just be a family money transfer unrelated to business. Utility payment might be consistent because the bill is paid from a joint account, not necessarily the borrower’s income.

More critically, algorithmic bias risks disproportionately excluding underrepresented groups. If the training data has few low-income women borrowers, the algorithm might learn patterns that disadvantage women. If rural data is sparse, rural borrowers might be systematically underscored.

Solutions Emerging:

- Explicit fairness constraints in model training (test for bias across demographic groups)

- Diverse training data (actively including underrepresented groups)

- Bias auditing and monitoring (continuous checking for discrimination)

- Explainability requirements (ability to explain why someone was approved/rejected)

- Human review of borderline cases (automation plus human judgment)

Challenge 3: Digital Literacy and Access

For AI credit scoring to work, people need digital access—smartphones, internet, ability to use apps. Digital literacy gaps might prevent access for those without education.

Solutions Emerging:

- Simplified interfaces designed for non-technical users

- Voice-based access (speak questions, hear answers)

- Community health worker assistance (NGO staff helping community members navigate apps)

- Feature phones support (SMS-based access for those without smartphones)

- Progressive disclosure (simple interface with options for advanced users)

Challenge 4: Regulatory Uncertainty

Governments struggle with AI credit scoring regulation. How much data can be collected? How can privacy be protected? What transparency is required? Without clear rules, fintech companies face legal uncertainty.

Solutions Emerging:

- Government frameworks (Egypt’s Personal Data Protection Law, India’s data governance experiments)

- Central bank oversight (Philippines’ BSP Online Buddy chatbot for consumer complaints)

- International standards (emerging fintech regulation best practices)

- Industry self-regulation (responsible AI principles adopted by leading companies)

Responsible AI: Not All AI Credit Scoring Is Fair

A critical point: AI credit scoring can reproduce or amplify inequality if not carefully designed.

Risk 1: Algorithmic Bias If training data reflects historical discrimination, the algorithm learns discrimination. An algorithm trained on data where women were historically rejected might learn to systematically reject women—now with mathematical authority.

Risk 2: Data Availability Bias Poor, rural, or marginalized groups generate less digital data. An algorithm learns from abundant data on urban, connected populations and performs poorly for rural users who generated sparse training data.

Risk 3: Predatory Lending at Scale AI enables approval at scale, potentially enabling predatory lenders to reach more vulnerable people. High-interest loans delivered algorithmically don’t stop being predatory.

Responsible AI Framework (MNT-Halan Model):

- Fairness First: Explicitly design models to include unbanked users; continuously test for bias

- Transparency: Users understand scoring factors; decisions are explainable

- Privacy: Data collected with consent; user control over data

- Continuous Monitoring: Track actual outcomes; retrain when bias detected

- Human Oversight: Sensitive decisions reviewed by humans; automation assists but doesn’t replace judgment

- Consumer Protection: Clear terms; reasonable interest rates; complaint mechanisms

- Financial Literacy: Education integrated into platform; users understand credit concepts

Responsible AI credit scoring expands opportunity without exploiting vulnerability.

Looking Forward: The Future of AI Credit Scoring

Current systems are impressive. Future systems will be transformative.

Credit Scoring 2.0: Behavioral Understanding

Next-generation systems will understand not just transaction patterns but behavioral context. A person’s savings pattern during harvest season might predict seasonal cash flow better than annual patterns. An e-commerce seller’s transaction spike before holidays might predict inventory management behavior.

Graduation and Dynamic Scoring

Instead of static scores, dynamic systems adjust scores based on recent behavior. A borrower with one successful repayment isn’t locked into “low creditworthiness”—their score improves with demonstrated success. This encourages graduation to larger loans and better credit terms.

Integration with Non-Financial Services

Credit scoring combined with:

- Agricultural advice (optimal planting, pest management)

- Health insurance (integrated health + financial security)

- Education financing (loans for skill-building)

- Business coaching (improving business practices)

This integrated approach addresses the complete picture of why someone’s business might succeed or fail.

Predictive Career Development

Rather than just approving credit, systems predict what support would help someone succeed. A potential borrower might get matched with:

- Business training matched to their business type

- Peer groups of similar entrepreneurs (community and accountability)

- Mentor relationships with successful entrepreneurs

- Market information guiding business decisions

Conclusion: Financial Inclusion as Empowerment

For a billion people globally, access to capital has determined life trajectory. Without borrowing ability, ambition meets a wall. Talent can’t translate to opportunity. Entrepreneurship remains a dream rather than reality.

AI credit scoring breaks this barrier by proving that creditworthiness exists—with or without formal credit history. It extends to the previously excluded the same economic empowerment the wealthy take for granted: the ability to borrow against future earnings to invest in present opportunity.

The impact isn’t primarily about banks’ efficiency or financial inclusion metrics. It’s about human possibility. A woman who wanted to expand her business can now do so. A young man can start the company he envisioned. A farmer can invest in better equipment. Communities can transition from subsistence survival to genuine economic growth.

The evidence from Egypt, Kenya, India, and Indonesia shows this is working—at scale, with financial discipline, and with positive outcomes. 65 million people have accessed credit previously impossible to imagine. Their businesses are growing. Their incomes are rising. Their children are going to school.

AI credit scoring hasn’t solved poverty—poverty is complex. But it has solved one of poverty’s most fundamental barriers: access to capital. And for 1+ billion people, that changes everything.

Sources & References

-

1

weight — lankawebsites.com

Related Articles

Securing Remote Work and Hybrid Teams

Remote and hybrid work models have become the norm for many organisations across Sri Lanka, offering flexibility and broader talent access. Yet this distributed approach introduces significant securit

The Future of E-Commerce Web Design in Sri Lanka in 2026

Sri Lanka's e-commerce sector is booming, with online sales projected to surge thanks to rising internet access and shifting consumer habits. As we step into 2026, e-commerce web design isn't just abo

Mobile-First Website Trends in Sri Lanka for 2026

Sri Lanka's digital landscape is exploding, with over 13.9 million of us online and mobile devices ruling our daily lives.Mobile-first website trends in Sri Lanka for 2026 aren't just a buzzword—they'

Website Redesign Checklist for Sri Lankan SMEs in 2026

In 2026, your website isn't just a digital brochure—it's your SME's frontline salesperson, lead generator, and trust builder in Sri Lanka's competitive online landscape. With over 70% of local custome